The Great Divergence

The Great Divergence

Is the world ready to leave the key success factor for economic and social progress behind?

Cooperation has been the single most important force for economic progress and prosperity. Developing specialized technological know-how, leveraging resources, and exchanging goods and ideas on international markets has increased the income and wealth of countries which participated in this virtuous cycle. After the Second World War, the Bretton Woods system, the International Monetary Fund (IMF), and the World Bank were created specifically to rebuild the world in an economic system of save cooperation and exchange, and the world entered a period in which living standards improved dramatically for almost 80 years.

As wealth increased, so did anxiety to protect it. The richer entire countries became, the more they had to lose. To some degree, it is a natural instinct. When you perceive danger, you tend to cave in, fortify, and build moats. The global Covid pandemic exposed that the world had become more vulnerable to economic shocks. In some cases, it was the dependency on single resources, in other cases, a dependency on single countries. In one instance, it was a single trade route which turned out to have become a bottleneck in global trade, when a container ship ran aground in the Suez Canal and blocked it for several weeks.

As countries are sorting out their risks and cleaning up their dependencies, the pendulum of global integration is swinging back. As it gathers momentum, there will be collateral damage and undesired side-effects. Time for a quick check on the state of affairs.

Pulling out the bazooka

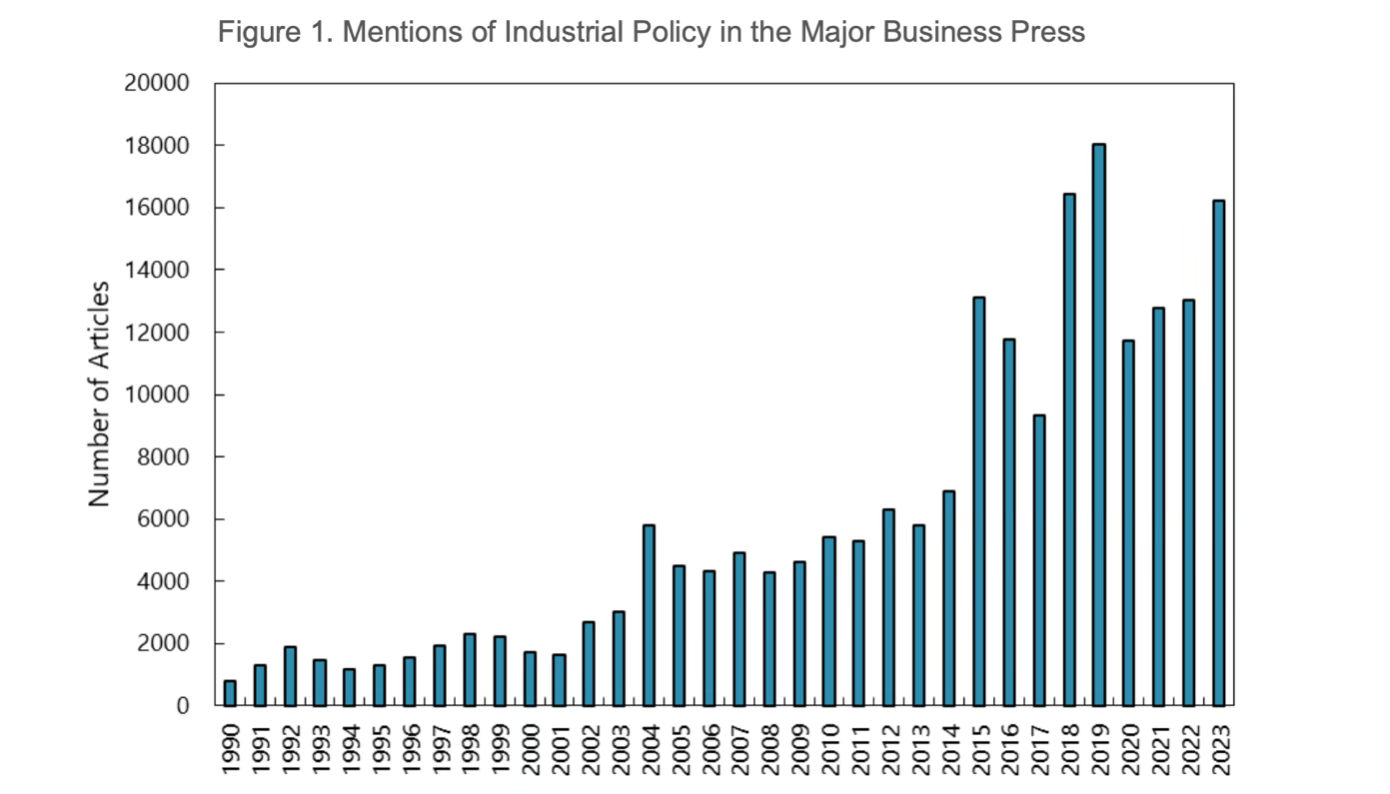

That something is going on in international trade has long been reflected in news reporting. Public discussions about trade restrictions and strategic support for specific economic sectors have been rising in recent years and already before Covid and Russia’s invasion of the Ukraine.

How did those discussions translate into action? Was it just talk, or also walk? Economists at the IMF rolled up their sleeves and dug deep into the bureaucratic underpinnings of international relations and trade to check if there’s evidence for increasing hurdles for global cooperation1.

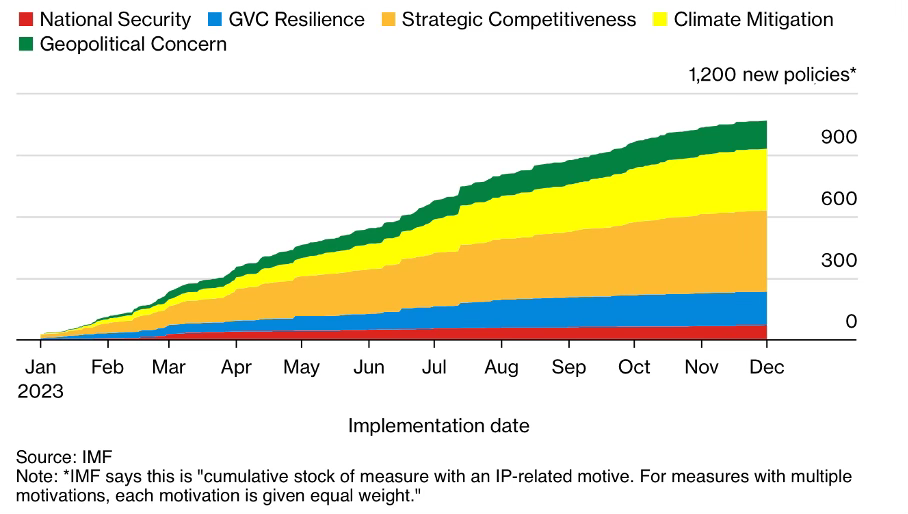

Their findings were sobering. They show that indeed, we’re going through a clear resurgence of industrial policy, a massive wave of new government policies in a mix of subsidies, embargoes, and tariffs. The dominating driver of industrial policy, according to the IMF research, is strategic competitiveness.

Historically, trade policy was driven by special-interest groups who typically claimed they suffered from unfair foreign competition. They pushed their representatives, politicians or trade associations, to protect them from foreign competition through import tariffs, or even better, subsidies. In recent years however it was the general public who has been pressing for a new category of industrial policy, broadly termed “climate mitigation”. That category has quickly taken a solid second place in global policies. But just like all other forms of interventions, it is going to benefit specific companies.

Beware of good intentions

Climate policies are a particularly good example to demonstrate how easily the borders between good intentions and old-fashioned protectionism blur. In August 2022, the U.S. Congress passed the Inflation Reduction Act (IRA) to support climate protection initiatives, energy security, and other policies. A whopping $369 billion were earmarked as subsidies for electric vehicles and other clean technologies under the IRA. Consumers can get a tax break of $7,500 when they buy an EV, but here comes the snag: the vehicles’ final assembly must take place in North America, plus at least half of the value of batteries, the biggest cost component, must be manufactured there as well.

Of course, European car makers were quick to cry foul. In January 2023, the European Commission presented its Green Deal Industrial Plan to help European companies in competition for clean tech products. But in contrast to the U.S., Europe does not have federal financing for such plans, and bickering started soon about which country contributes how much to any such plan, and how much they can draw from it.

The IRA and Europe’s Green Deal are textbook examples of another key finding of the IMF study. The researchers showed that once a country imposed a policy to support a given sector or product, there is a 74% probability that other countries will respond with competing subsidies within a year. Clearly there is a strong dynamic for escalation in industrial policies which is very hard to break once unleashed.

(Unloading relations: The Boston Tea Party, pictured in W. D. Cooper’s The History of North America)

Building trenches around emerging key technologies

Economists in general dislike industrial policies. They point out that they usually just lead to higher prices for consumers, a lack of innovation, and in the end to declining competitiveness. But today we’re looking at a situation which maybe does need some level of government intervention. The current approach for AI development requires resources at a super-large scale: data centers with hundreds of thousands, or even millions of GPUs costing tens of billions of dollars (the Stargate data center cluster of OpenAI and Microsoft supposedly has a price tag of $100 billion), and an energy consumption equivalent to what large nuclear power plants produce.

Realizing the potential of AI after witnessing the generative-AI breakthroughs at OpenAI and Google, the U.S. launched a clear strategy to build leadership in AI development. Under president Joe Biden, the U.S. passed the CHIPS act, an initiative to rebuild chipmaking capabilities. Let’s not forget that U.S. company Intel was the leading global developer and producer of microchips for decades, setting the benchmarks for speed and production scale. Intel was accompanied by smaller companies such as AMD or Apple Computers. However, in the mid-2010s Intel missed the transition to “extreme ultraviolet lithography”, the technology to print wiring on microchip wavers on a nanometer scale. On current 2-nanometer wavers, wiring has a width of less than 10 atoms. Technological leadership in chip production went to Taiwan.

With the CHIPS act, the U.S. intends to take production back on home soil. In March 2024, Intel was awarded a grant of $8.5 billion, and a low-cost government loan of $11 billion, to build manufacturing in Arizona. “If we invented it in America, it should be made in America”, U.S. president Biden said during the announcement of the grant.

Three weeks later, in early April, the administration announced a subsidy to Taiwan Semiconductor Manufacturing Co (TSMC), worth $6.6 billion and a government loan of $5 billion. TSMC agreed to expand investment in the U.S. by $25 billion, to $65 billion, to build a third microchip plant near Phenix, Arizona.

Europe stood by and watched in disbelief what was happening in the U.S. Finally the EU announced its own program, creatively called the EU Chips Act, with the questionable target to double the output of the EU’s chipmaking to 20% of global production.

In July 2023, the German government said it was going to fund the program with €20 billion to support domestic champion Infineon, but also Intel and TSMC which both expressed interest to invest in a tech cluster at Magdeburg. Germany intended to take the money from its “Climate and Transformation Fund”. But the government received a heavy punch in the solar plexus. The country’s Federal Constitutional Court ruled in November 2023 that a large component of the Climate and Transformation Fund was an illegal circumvention of debt ceiling rules, essentially shutting it down and forcing the government to impose an emergency spending freeze. The impact on the green transition has been widely reported. The fund was supposed to finance homebuilders’ investments in heat pumps, and industrial companies’ transition to renewable sources of energy. Both initiatives are in a limbo now. Typical for government-sponsored investments, they don’t make commercial sense without the subsidies.

But in the clutter of green transition, the impact on Germany’s technology industry has been missed. Without Germany’s financial and engineering leadership, the EU’s microchip “strategy” isn’t going anywhere.

This is even more surprising (or frustrating, depending on the perspective) considering that Europe is home to the bedrock of semiconductor technology: ASML (Advanced Semiconductor Materials Lithography, though the company doesn’t use that long-form name anymore) of the Netherlands, which developed and owns extreme ultraviolet lithography. It produces the machines for chip manufacturing and is a key supplier for TSMC.

While the Climate and Transformation Fund was an almost laughable fail, Europe and in particular Germany are facing another large hurdle in AI development: energy. Training of AI models is notoriously energy intensive. Microsoft and OpenAI are understood to be building new datacenters for the next development phase of AI. Neither Microsoft nor OpenAI offered any details on the plan, but it is expected that they will feature at least a million GPUs and XPUs (an XPU integrates a CPU and a GPU).

Let’s quickly run some numbers. A single Nvidia H100-SXM GPU pulls up to 700 watts of electrical power. To be conservative, let’s use 500 watts. For a million units, that’s 500 megawatts, which is the output of a large nuclear power plant.

Where would the energy come from for a similar datacenter cluster in Europe? Germany has the engineering capabilities, but its power grid is already being stretched to its limits by two opposing forces, the transition to volatile sources of renewable energy (wind, solar) on the supply side, and a huge increase in demand from heat pumps (at least 65% of total energy consumption for new houses has to be renewable) and industry, plus the electrification of the car fleet. In early March 2024, the government’s auditor issued a scathing report to the German government for its failures in the energy transition, mentioning specifically vulnerabilities of the electrical grid (more on Germany’s grid troubles here).

How does China stack up?

The Chinese government announced its own development fund of semiconductors, budgeted around $30 billion. But China’s position is even worse than Europe’s. Both the U.S. and the EU have imposed restrictions on the sale of advanced microchips and machinery to China, so China can’t get its hands on either chips or manufacturing equipment like ASML’s fab machines.

The government has ordered its large telecom equipment companies like Huawei to source microchips from Chinese firms to provide some scale to local producers. It’s true that just a few years ago, China was considered a leader in AI development, and the country filed the largest number of AI patents. But AI development has taken a different direction. Researchers at Google and OpenAI have developed the math and computational architecture for AI, and Nvidia the computing power. China will have to start from scratch but is largely cut off from international cooperation and development. The country will have to replicate technologies which took decades to develop, huge amounts of capital, and cooperation across many countries. That’s already not the best position to begin with.

However China’s problems are much deeper. China’s past rapid technological progress was driven to some degree by the know-how it gained in joint ventures with international partners, and dubious programs as the “1000 talents plan”. Western companies have woken up to this threat.

Foreign direct investment has dropped to a 30-year low, as international companies have become more sensitive to the unwanted transfer of intellectual property, rising labor costs, increasing legal risks for foreign nationals, and geopolitical risks from China’s threat to Taiwan (for a detailed discussion on China please see here).

It is a first in peace times that the economic integration between large economic blocs unravels. If current trends persist, the past success drivers for China will dissipate. The enormity of that transition probably hasn’t been widely understood.

A new three-speed order?

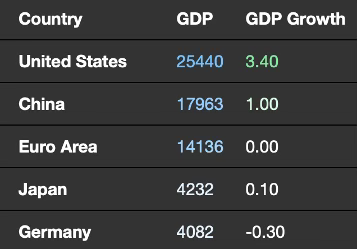

(snapshot of the most recent reported growth rates of main economic regions/ countries)

We’ve seen two fundamental forces emerge in the last few years, a technological revolution and the rise of industrial policy. In combination, those forces have the potential to lead to a divergence of the economic development of the main geopolitical/ economic regions into a three-speed world. Policymakers will have to ask themselves if this is a desired outcome, or if they want to counteract.

In speed group 1, there are the U.S. and countries in its sphere. The U.S. has the resources and technological leadership for AI development, and it seems it has found a robust strategy to defend and enhance its leadership. I’d still like to point out that the fiscal position is a significant weakness which can quickly become a huge distractor for the economic performance.

Group 2, Europe and allies. Europe in principle has the engineering capabilities for chip production, and it owns the key technology for advanced microchip production. But none of the European tech companies has remotely the scale needed for AI development. Microsoft, Apple, and Nvidia each are fifteen times larger than the biggest European tech firm. Even French luxury goods firm Hermès is more than twice the size of SAP, Germany’s largest company.

And equally important, critical parts of Europe are caught up in an ever more bizarre transition to renewable energy. Accordingly, in the emerging trade war the European Commission identified the following items as strategic equipment: batteries, solar panels, wind turbines, and heat pumps.

To avoid falling further behind the U.S., Europe will have to consider if it has the priorities right, how to sort out the energy mess, and find ways to more effectively align internally among member countries.Group 3, China and its allies including Iran and Russia. Historically countries, including China, experienced their most successful development through increasing trade, higher investments, more integration. But China is diverging from the common development track with the U.S. and the EU and gravitates towards pariah states. Unless the country course-corrects decidedly I think it will be very difficult to extend the impressive growth story.

As always, curious to hear your thoughts!

All the best,

John

“The Return of Industrial Policy in Data”, IMF Working Paper, January 2024

I know the IMFs report is backward looking but I think there might be a departure very soon from one of their conclusions, namely that its mainly less developed countries that implement trade restrictions.

The EU’s Carbon Border Adjustment Mechanism (CBAM) requires importers purchase certificates based on the volume of carbon intensive products and the independently-verified emissions content of those goods. The levy will be introduced in 2026, gradually phased in at the same rate that free allocations for obligated emitters in the EU are withdrawn. By 2034 importers will have to pay 100% of the CBAM cost.

Other developed economies including the UK, Australia, the US, and Australia are already considering their own carbon border levy. Crucially the EU's CBAM is only payable if the production country-of-origin does not have a comparable carbon price as the EU’s. The EU’s CBAM will initially cover imports of iron and steel, cement, fertiliser, aluminium, electricity, and hydrogen. Nevertheless, all sectors covered by the EU ETS are thought likely to be subject to the CBAM by 2030, or very soon afterward.

The upshot of the policy is that those countries most exposed to the CBAM are starting to ramp up their own carbon compliance schemes, including China, Turkey, India, etc.