The Three Trillion Dollar Trap

The Fed’s new chairman has much bigger tasks ahead than rates decisions

Dear readers,

Central banking might not sound like the most captivating topic in the world. But the policies implemented after the Global Financial Crisis explain much of the deeply worrying state of western financial markets – from absurd valuations of stock exchange indices and IPOs to unaffordable housing and inflation rates which make everyday shopping a distressing experience. High time for Kevin Warsh to address a persistent problem.

The U.S. Federal Reserve just finished its first FOMC meeting (Federal Open Market Committee, the body which decides on policy interest rates) under the Fed’s new chairman Kevin Warsh. The federal funds rate was left unchanged in a target corridor of 3.5%-3.75%, as widely expected. Warsh will change a few other items – fewer comments on the economic outlook, and he decided to scrap “forward guidance”, i.e. comments on the likely future course of monetary policy. All of that is just the daily hustle of central banking, an endless iteration of tactical decisions. Nothing that leaves a heritage as a great economist.

But Warsh has something else in mind. What he really wants: unravel the biggest experiment in monetary economics in modern history, the policy which created many of today’s imbalances in the financial system and inflation rates which have impoverished large parts of the populations in all countries which followed this policy.

If you’ve followed me for a while, you know I’m very critical of the approach western central banks have taken after the Global Financial Crisis – in fact it’s my core thesis why all those imbalances in our economic system have developed.

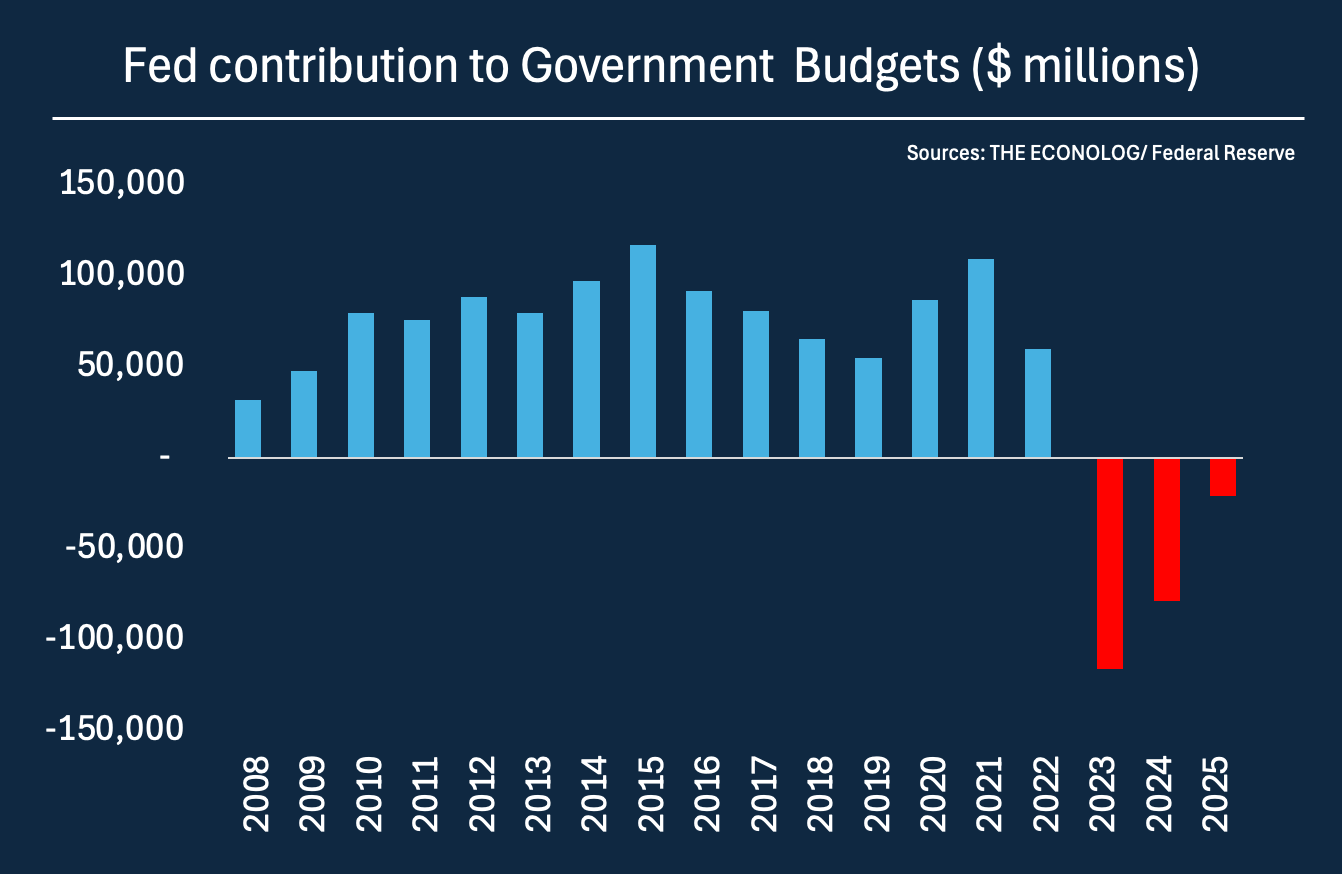

Here’s a quick summary just as a reminder. After the GFC, the Federal Reserve realized the financial system had gone through three shock events in just ten years, all of which resulted in liquidity crises in the banking system. In each case, market liquidity dried out, and during the GFC, banks stopped lending to other banks, the worst-case scenario for financial economies. The obvious solution? Provide more liquidity than banks would ever need. The U.S. Federal Reserve therefore implemented a new approach for monetary policy called “ample reserves”. It bought Treasury bonds and mortgage-backed securities which it paid with fresh central bank money in several rounds of quantitative easing. In mid-2008, the Fed’s bond portfolio amounted to about $800 billion, built over almost 100 years to increase money supply gradually. At the end of 2021, just thirteen years later, the portfolio had expanded to almost $9 trillion.

The new policy had a nice and widely underappreciated feature. The Federal Reserve received income from the bonds which it is obliged to pass on to the U.S. Treasury. A very convenient setup, because in the end the Treasury was paying interest on its bonds to itself. Over the years, remittances to the Treasury summed up to over 1 trillion dollars.

But the policy also led to an astronomical increase in money supply, warped asset prices and yield curves, and inflation in consumer goods.

Keep reading with a 7-day free trial

Subscribe to The Econolog to keep reading this post and get 7 days of free access to the full post archives.